Case Study / Student Loans

The Architect’s Guide to Outsmarting Student Debt

When student loans span multiple interest rates, providers, and payment brackets, budgeting feels less like math and more like managing a slow, permanent leak.

For high-achieving professionals, the weight of student loans isn’t just about the balance sheet—it is about the compounding cognitive load. Balancing federal Direct subsidized loans with higher-interest graduate PLUS loans creates a constant state of calculation fatigue. Traditional personal finance software tells you where the money went last month, but leaves you to design the path forward in your head. LEVEL changes the paradigm by moving you from a defensive, reactive stance to a structural strategy.

Step 1: Out of the Inbox, Into the Wizard

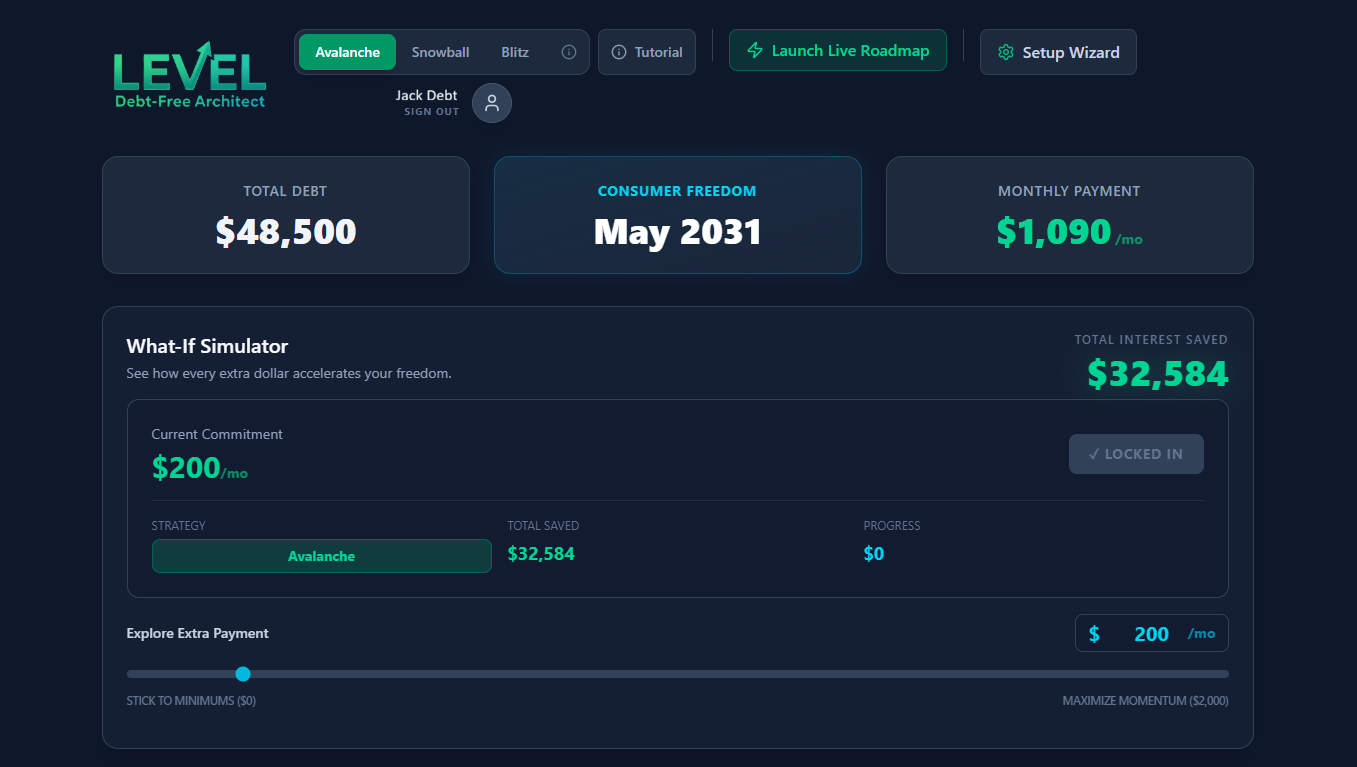

The first step toward time autonomy is centralizing your targets. LEVEL’s onboarding wizard doesn’t force you into complex manual spreadsheets. You simply list your balances, interest rates, and minimums. The interface gathers these disparate entries, transforming your stack of individual servicer balances into a unified dashboard.

Once your accounts are initialized, the wizard asks you to select a payoff framework. Rather than forcing you to guess the math, the tool compares classic methodologies side by side. For student loans, where interest rates fluctuate between low undergraduate loans and high graduate notes, selecting the right routing makes a massive financial impact.

Interest-Focused Routing

The Avalanche Strategy

Directs surplus payments to the highest-interest loans first, mathematically minimizing your interest bleed over time.

Psychology-Focused Routing

The Snowball Strategy

Targets the smallest total balances first. Delivers fast, immediate mental wins to clear entire loans off your plate.

Step 2: Simulating “What-If” Scenarios

When you secure a raise, a bonus, or adjust your lifestyle, you shouldn’t have to guess what that means for your future. The tracking trap of traditional tools keeps you focused on past transactions. LEVEL’s “what-if” simulator is built to help you project future changes instantly.

Using the simulator, you can toggle additional monthly payments or experiment with lump-sum injections (like tax refunds). The interface updates your payoff date and overall interest cost in real time. It shifts your mindset from “How much do I owe?” to “How quickly can I buy back my time?”

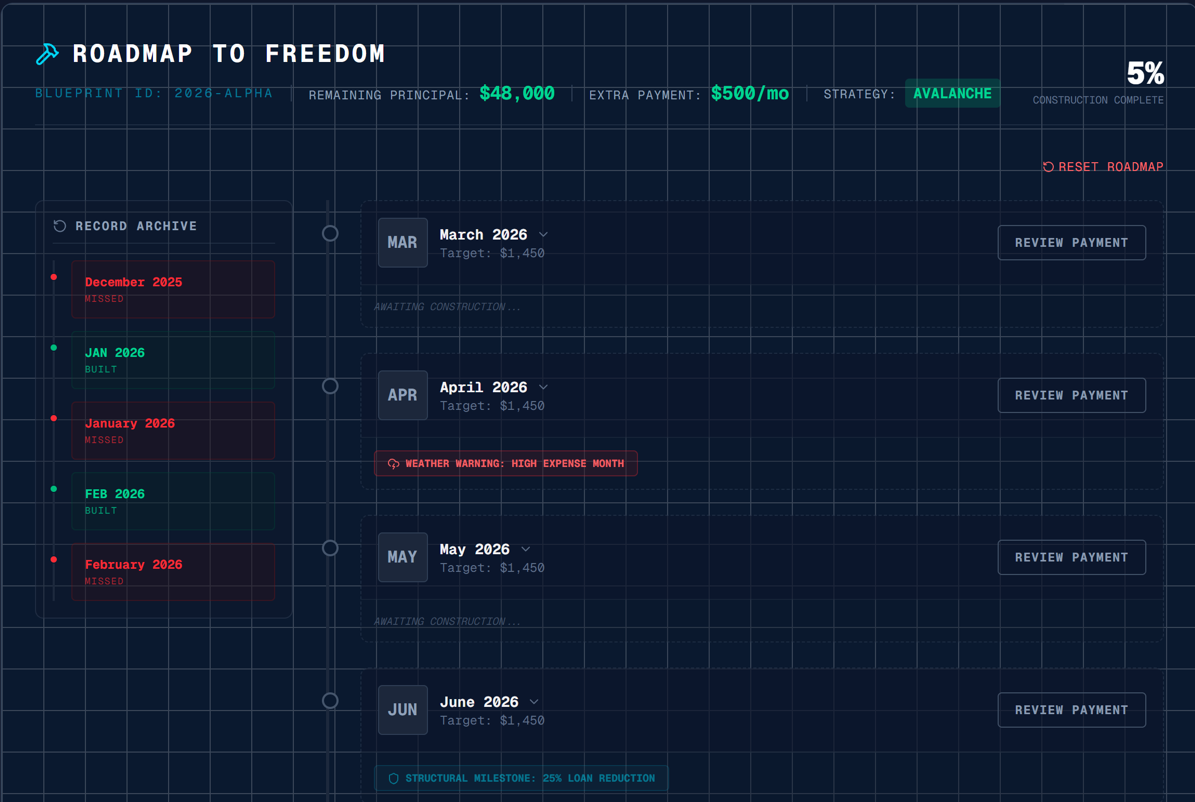

Step 3: Following the Live Roadmap

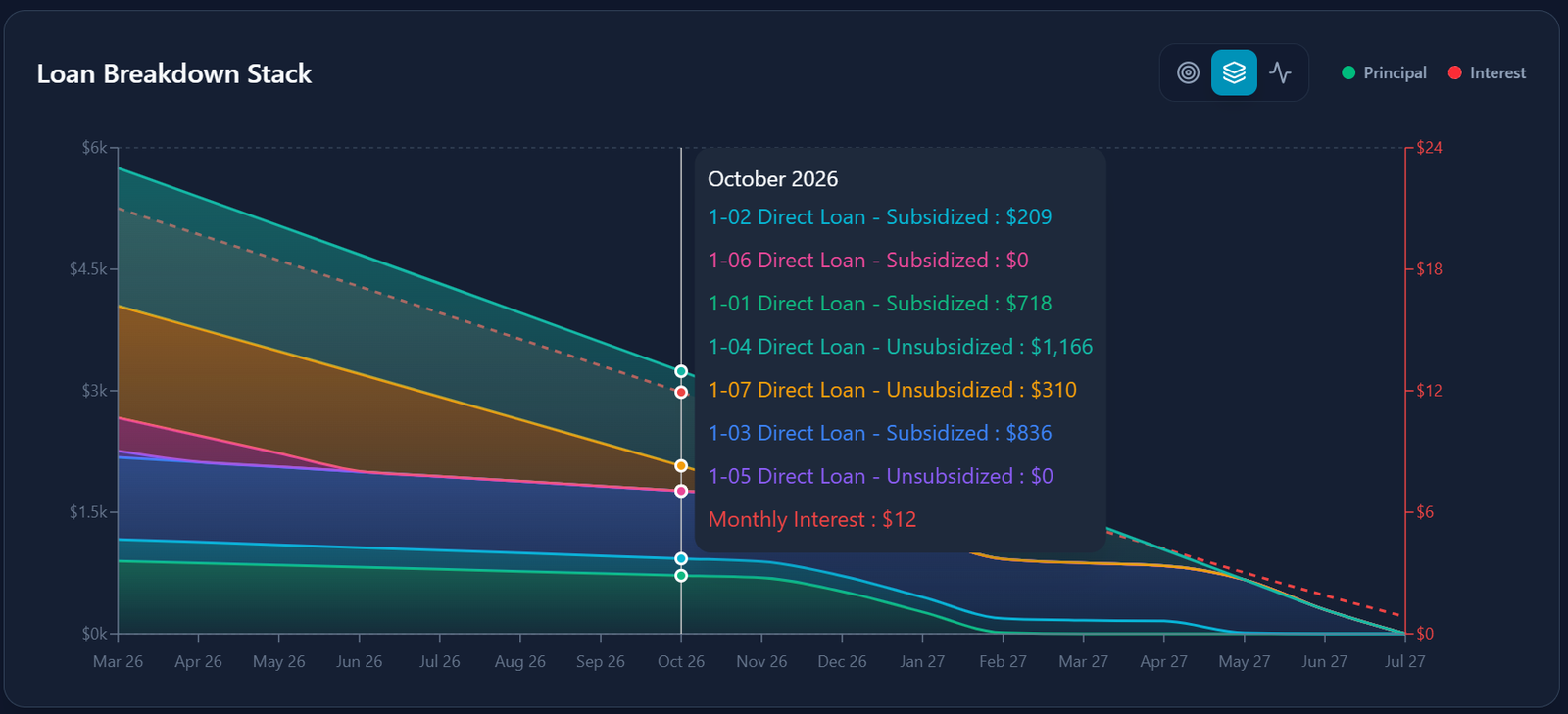

With your strategy locked in, LEVEL generates a live roadmap. This active interface guides your payments month by month, telling you precisely where to direct any surplus income to maintain peak momentum. Instead of logging into three different student loan portals to guess your extra payments, you simply open your roadmap, review your targets, and check off the milestone.

Onboard the Portfolio

Consolidate federal, private, and graduate loans in under five minutes using our streamlined setup wizard.

Run Future Simulations

Test monthly surplus variations to locate the tipping point where your interest bleed drops off drastically.

Execute Month-by-Month

Follow the dynamic monthly roadmap, marking off milestones as each balance drops off the board.

Should I pay off my lowest balance or highest interest student loan first?

Does LEVEL support federal income-driven repayment (IDR) plans?

What is the benefit of the PDF Blueprint feature?

Take Back Your Time

Your student loans shouldn’t act as a permanent ceiling on your life choices.

Stop managing spreadsheets and start building an intentional strategy. End the financial burnout with LEVEL ↗