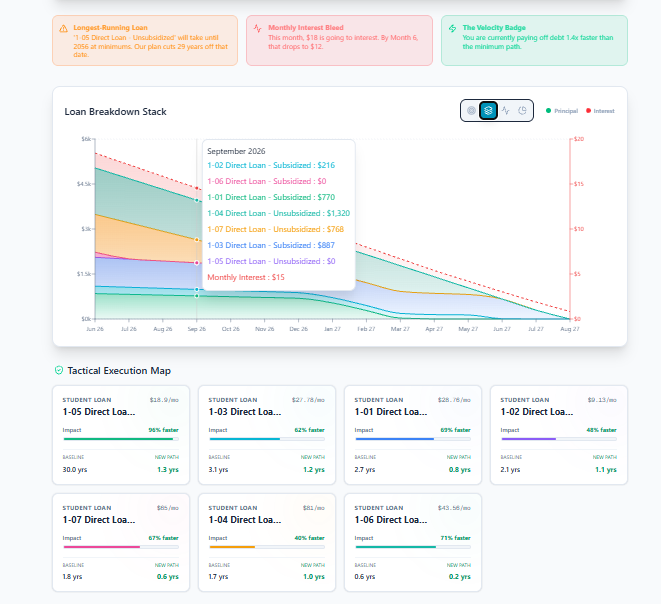

Payoff Methodologies

Comparing LEVEL Payoff Strategies: Avalanche, Snowball, Blitz, and Custom

When structuring a debt payoff, there is no one-size-fits-all solution. LEVEL’s routing engine supports four core strategic paths—Avalanche, Snowball, Dynamic Blitz, and Custom Sequence—allowing you to prioritize psychological speed or pure mathematical optimization.

Rigid personal finance programs force you to follow a single method. This lack of choice leads to financial burnout when high balances stagnate under Snowball, or motivational fatigue sets in under Avalanche. By analyzing the mathematical behavior of each routing algorithm, you can match your payoff strategy to your immediate cash flow needs, minimizing the mental weight of decision fatigue. Below, we break down each framework in detail.

- Snowball: Targets the smallest balance first (optimizes psychological momentum).

- Avalanche: Targets the highest interest rate/APR first (optimizes lifetime mathematical savings).

- Dynamic Blitz: Targets the highest absolute monthly interest dollars (optimizes immediate cash flow recovery).

- Custom: Let’s you manually sequence loans according to your own custom rules.

1. The Snowball Method: Psychological Acceleration

The Snowball method sorts your debts strictly from the smallest outstanding balance to the largest. Your interest rates are ignored for ranking; extra payments target the tiny accounts first to get them off your ledger as fast as possible.

By clearing small accounts quickly, you secure quick wins. Wiping out a minor $300 balance in the first month builds behavioral motivation and frees up that specific minimum payment to roll into the next account in your stack. This approach is best for individuals who need instant positive reinforcement to stay committed to a long-term plan.

2. The Avalanche Method: Mathematical Perfection

The Avalanche method sorts debts by their interest rate (APR), focusing all principal acceleration on the highest-rate account first. Balances are completely ignored in this sorting order.

Mathematically, this is the most efficient path. By attacking high-rate liabilities first, you prevent interest from compounding, saving the largest amount of absolute money over the life of your plan. This strategy is ideal for numbers-driven individuals who prioritize long-term interest minimization above short-term psychological rewards.

Traditional Stack

Snowball vs. Avalanche

Snowball focuses entirely on account volume, maximizing motivation through fast wins. Avalanche focuses entirely on interest rates, minimizing total lifetime cash outlay.

LEVEL Hybrid Stack

Dynamic Blitz vs. Custom

Dynamic Blitz targets absolute monthly dollar bleed (Balance × APR) to protect cash flow first. Custom Sequence lets you rank accounts manually based on personal values.

3. The Dynamic Blitz Method: Cash Flow Protection

LEVEL’s signature Blitz method targets the account causing the most immediate cash bleed to your monthly household budget. It calculates this by multiplying each balance by its interest rate to find the absolute dollar interest generated each month (Balance × APR / 12).

This hybrid algorithm is highly effective for large balances. Often, a mid-rate account with a massive balance generates far more actual dollar interest than a tiny account with a high rate. Wiping out the largest monthly dollar drain releases cash flow back into your budget faster, providing immediate, tangible relief to your monthly ledger.

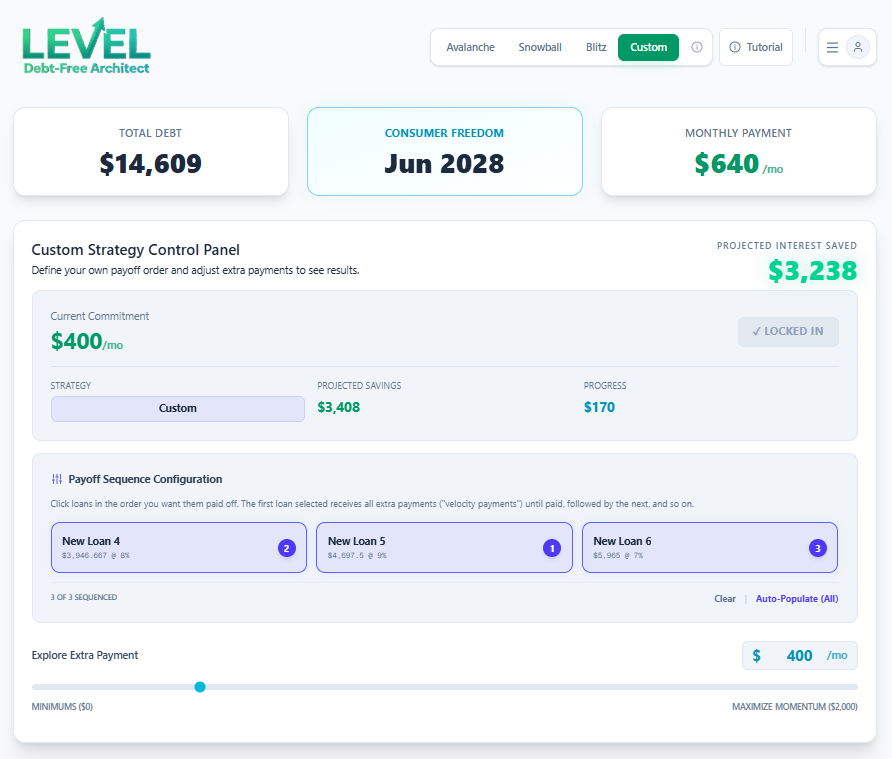

4. The Custom Sequence Method: Personal Autonomy

For individuals with unique obligations—such as family loans or accounts with looming promotion periods—LEVEL supports Custom Sequencing. You can manually drag and drop your loans from your dashboard to dictate the exact flow of your extra payments.

Custom sequencing is perfect for handling zero-interest intro periods. If a credit card has a 0% promotional rate expiring in six months, you can prioritize it at the top of your custom stack to ensure it is paid off before the interest penalty triggers, bypassing standard algorithm rules entirely.

Best Practices for Strategy Selection

To determine the best path for your unique situation, follow these guidelines:

- Assess Your Budget Flexibility: If your monthly cash flow is tight and you feel stressed by having multiple active minimum payments, start with the Snowball method to clear accounts quickly.

- Compare Projections on the Simulator: Use the What-If Simulator to swap strategies. Inspect the difference in total interest paid and target dates. If the mathematical difference is negligible, choose the strategy that aligns best with your behavior.

- Account for Intro Rates Manually: If you have promotional accounts, use a Custom Sequence to pay them off before their rates spike, protecting your ledger from sudden compounding penalties.

Frequently Asked Questions

Which payoff strategy saves the most money?

How is the Dynamic Blitz strategy different from the Avalanche strategy?

Can I mix strategies on LEVEL?

Select Your Blueprint

Don’t let rigid systems restrict your cash flow potential.

Stop managing rigid budgeting tools. Launch your custom payoff stack on LEVEL today ↗